The sharp rally followed by a deep correction seen in past cycles may not necessarily repeat, as gold is increasingly viewed as a strategic asset by countries seeking to reduce dependence on the US dollar, experts say.

Global gold prices have repeatedly set new records, surpassing USD 5,500 per ounce in early 2026 before correcting to around USD 5,000 in recent sessions. This morning, the precious metal climbed to a three-week high of USD 5,227. Over just three years, gold prices have tripled, significantly outpacing forecasts by major financial institutions.

Alongside the strong upward momentum, concerns are mounting that gold could face a sharp reversal after years of “overheated” gains. Over the past five decades, deep downturns followed two of the three major bull cycles in the gold market.

The year 1971 marked a watershed moment for the modern gold market, when the United States ended the gold standard, allowing the metal to trade freely based on global supply and demand. In the aftermath, gold prices surged tenfold between 1971 and 1980. However, as inflation was brought under control and global monetary policy tightened, prices fell sharply to less than half of their peak levels.

The second major upcycle took place from 2000 to 2011, amid a series of global economic and financial shocks, culminating in the 2008 financial crisis and the European sovereign debt crisis. Gold rose sevenfold over a decade before entering a four-year correction, declining 40% from its peak.

The third strong rally began in 2020, triggered by unprecedented global economic disruption caused by the Covid-19 pandemic. Unlike previous cycles, however, this uptrend did not end with a pronounced crash. Instead, it was extended by a renewed wave of gains beginning in 2022.

Speaking to VnExpress, Huynh Trung Khanh, Vice Chairman of the Vietnam Gold Traders Association (VGTA), said the current uptrend was activated in 2022 as geopolitical tensions escalated and the United States intensified economic sanctions.

Since then, the US dollar has increasingly been “weaponized” through sanctions and asset freezes, prompting many countries to restructure their reserve strategies.

The de-dollarization trend became more pronounced from 2022, particularly as Russia, China and BRICS nations accelerated shifts in reserves away from the US dollar and US Treasuries toward gold to safeguard their financial systems against geopolitical risks. Gold has emerged as a neutral alternative for central banks.

“Unlike previous cycles, gold in the current phase is not merely a store of value or short-term hedge, but is taking on a new role in national financial strategy,” Khanh said.

Against the backdrop of an expanding global fiat system underpinned by rising public debt, gold — finite in supply, impossible to print, and historically serving as a monetary anchor for thousands of years — is increasingly regarded as a strategic alternative asset. Persistent central bank purchases have become a key pillar supporting prices.

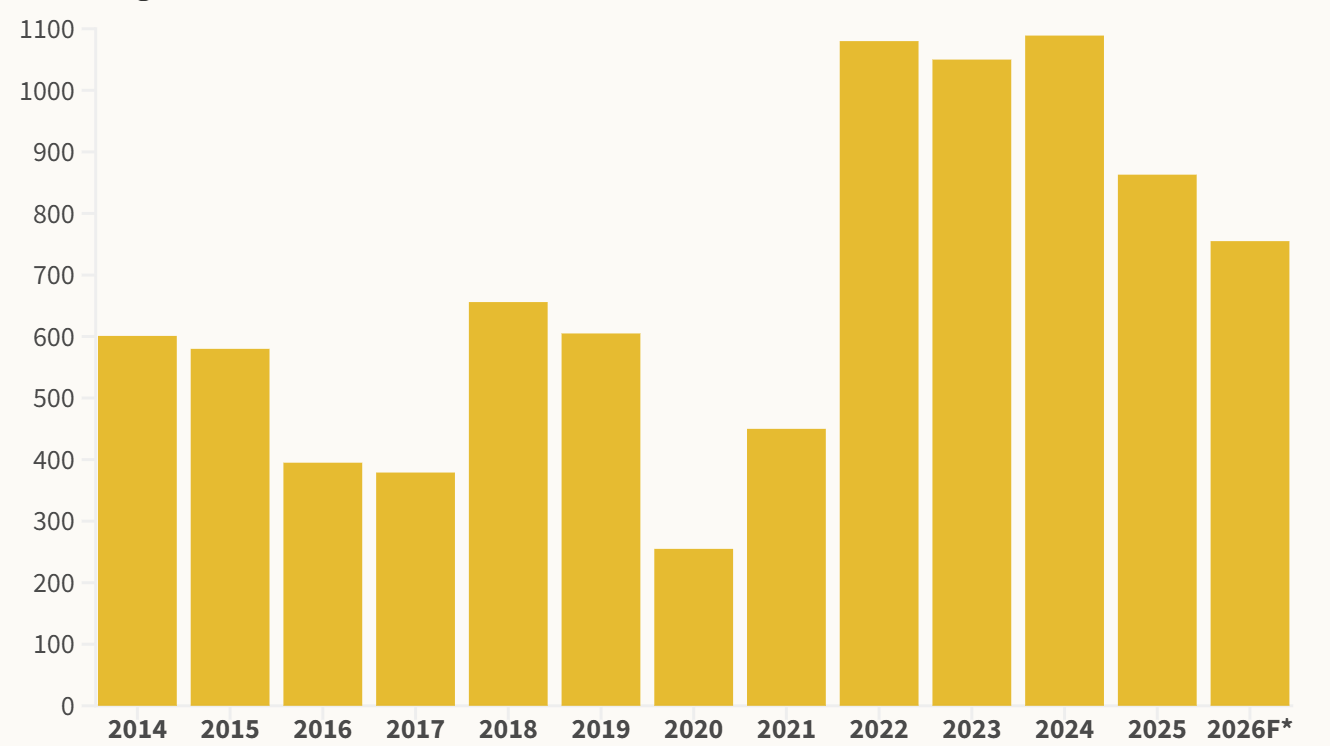

In contrast to two decades ago, when central banks were net sellers of gold, data from the World Gold Council show that since 2022 they have purchased roughly 1,000 tonnes annually, underscoring a fundamental shift in reserve management thinking.

David Einhorn, head of Greenlight Capital and widely known for his prescient short position against Lehman Brothers in 2008, said gold’s rally in recent years reflects its growing role as a reserve asset among central banks.

In an interview with CNBC, Einhorn argued that unstable US trade policies have prompted many countries to seek alternatives to the US dollar in settling international trade. Over the long term, he views holding gold as a rational strategy, citing what he described as a “meaningless” relationship between US fiscal and monetary policy, while noting that other major currencies are “just as bad or worse.”

The Official Monetary and Financial Institutions Forum (OMFIF) said recent geopolitical developments have laid a solid foundation for gold to “re-emerge prominently in central bank reserve portfolios, as well as a means of payment for certain countries.”

“The geopolitical and economic landscape has changed dramatically. As a result, traditional economic cycles may no longer fully repeat themselves. It is also very difficult to reverse the de-dollarization trend among central banks. Therefore, gold is becoming a strategic asset for nations, rather than merely a safe-haven channel for investors during periods of uncertainty,” Khanh said.